The Bright Side of Dark Markets: Experiments

Edward Halim, Yohanes E. Riyanto, Nilanjan Roy and Yan Wang

Abstract

We design an experiment to study the effects of dark trading on incentives to acquire costly information, price efficiency, market liquidity, and investors’ earnings in a financial market. When the information precision is high, adding a dark pool alongside a lit exchange encourages information acquisition, crowds out liquidity from the lit market, and results in a non-linear relationship between price efficiency and dark pool participation. At modest levels, dark pools enhance information aggregation. Investors with stronger signals use the lit exchange relatively more, and uninformed traders are better off when they trade more in the dark pool.

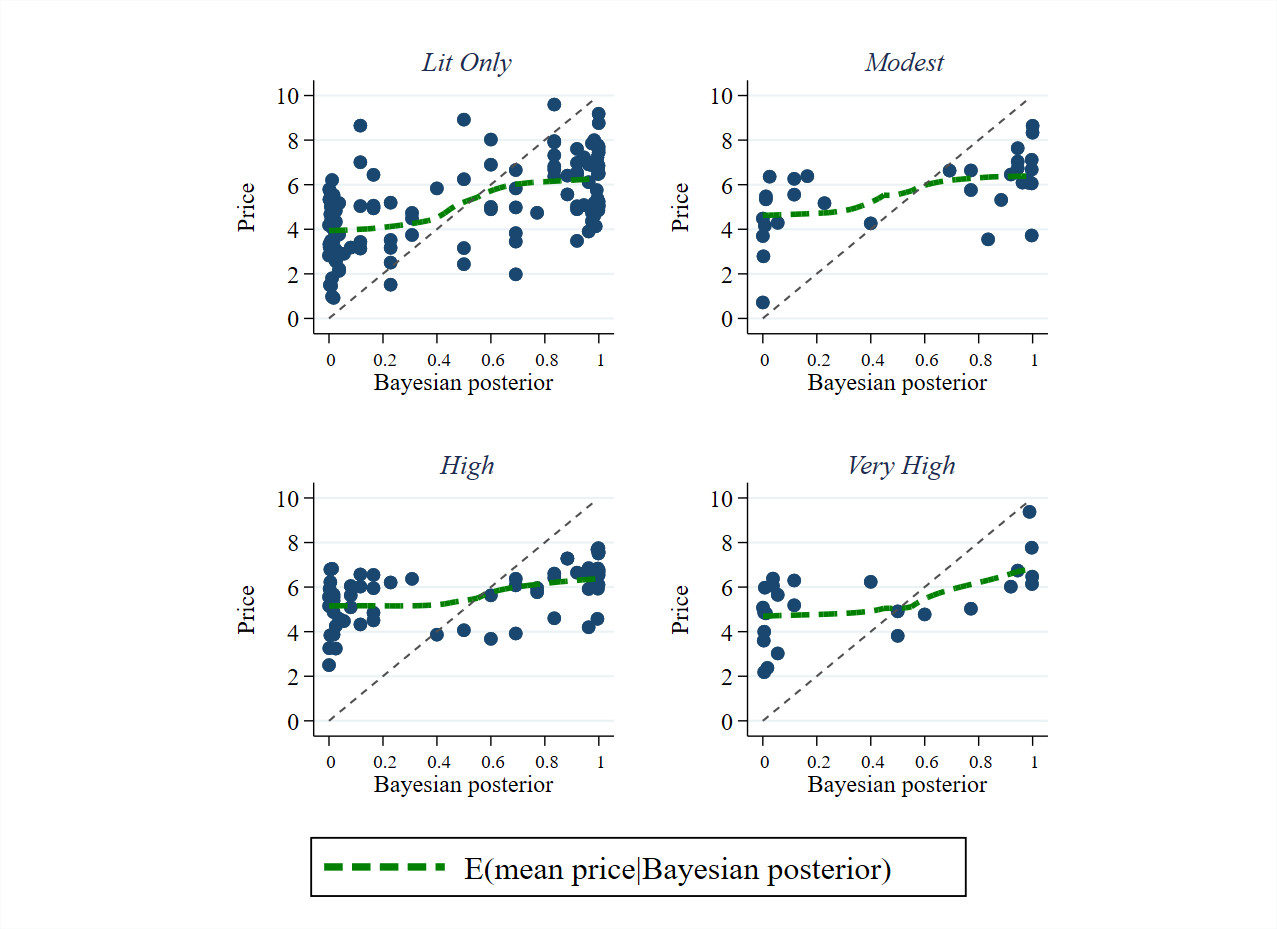

Figure 1: Precision of market prices in the lit market in Lit Only-Low and Dark-Low treatments

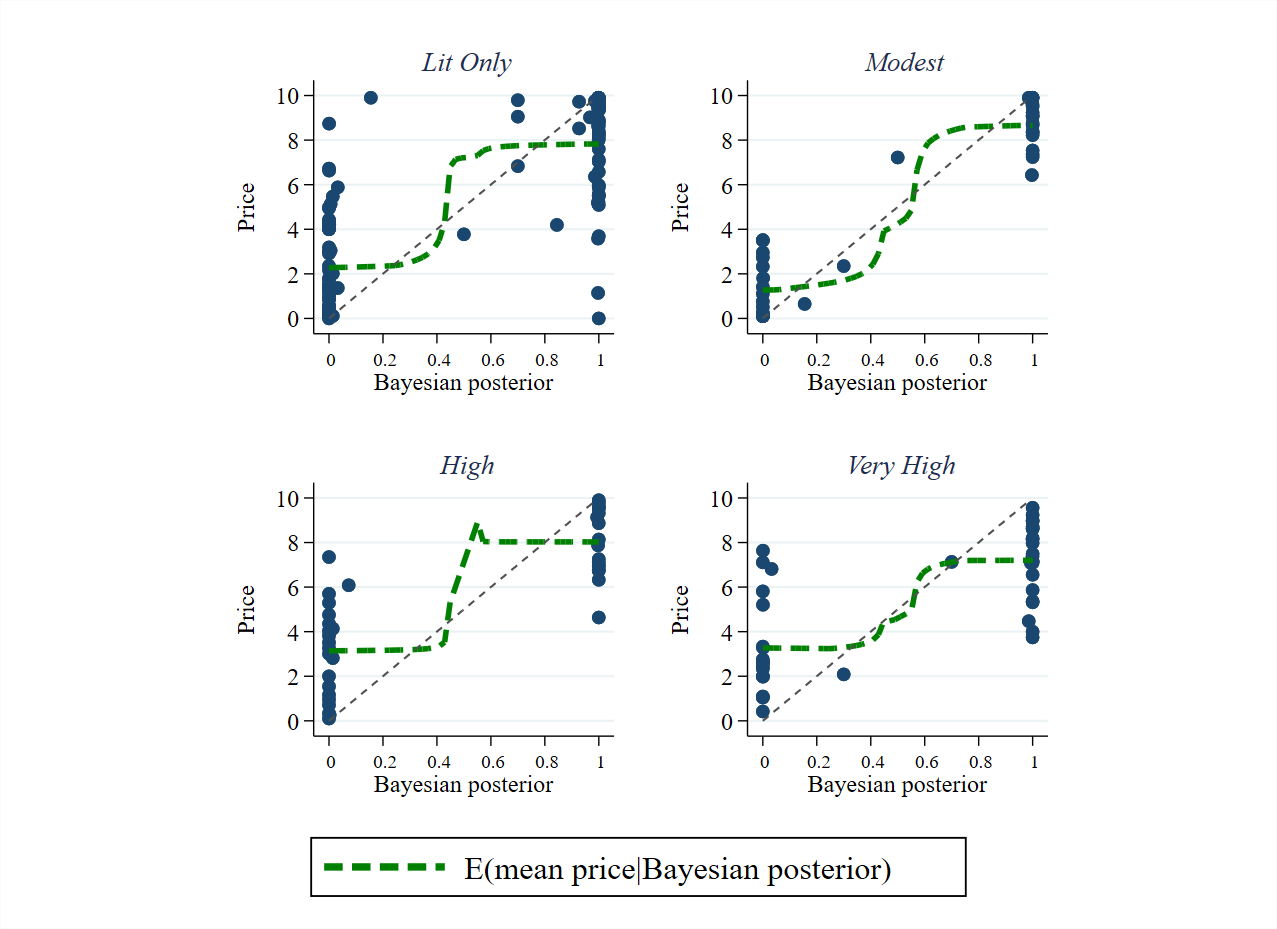

Figure 2: Precision of market prices in the lit market in Lit Only-High and Dark-High treatments

{kind=link}